Your Study Guide to Student Loan Forgiveness Programs

If you’re staring at a mountain of student loan debt, news of student loan forgiveness may sound too good to be true. But it doesn’t have to be. It won’t happen overnight, but there may be ways to work toward having all or part of your student loans forgiven.

First Things First

In this article we’ll focus on federal student loans. That accounts for the vast majority of student loans taken out in the United States and includes Perkins loans, Stafford loans, Federal Family Education Loan (FFEL) program loans, Direct Loans, Parent PLUS loans, Grad PLUS loans, and others. Student loans taken out through a bank or other private company won’t have these same options.

Almost all of the options described below come with a set of eligibility criteria. Those criteria might include the following details.

The year you took out your loan. Some student loan forgiveness programs are only eligible for loans taken out after a certain date, such as when the program was created.

The type of loan. Direct Loans qualify for most programs while Parent PLUS doesn’t qualify for many. It completely depends on the program though.

The school you attended or where you work. You will need to provide details about where you went to school when you took out the loan to apply for Closed School Discharge or Borrower Defense to Repayment. If you’re going for Public Service Loan Forgiveness or Teacher Loan Forgiveness you’ll need to work at qualifying institutions.

Your income. Three of the four income-driven repayment plans require your income to be below a certain level in order to qualify. The Revised Pay as you Earn (REPAYE) plan, however, is open to anyone.

Other program-specific qualifications. There are all sorts of other pieces of eligibility criteria for different programs. That’s why it’s important to thoroughly research your options to make sure you’re a candidate.

If your loans don’t qualify for the program that interests you, you may be able to consolidate into a new loan that does meet the qualifications. Direct Loan Consolidation is a process of rolling your existing loan or loans into one new loan. The original loan(s) is considered paid in full and a brand new loan is created. If your loans are too old to qualify for certain student loan forgiveness programs or if you have a mix of FFEL program loans and Direct loans, consolidation may work for you. As a bonus, you get to choose your servicer and you’ll have only one monthly payment to manage.

If you are planning to apply for a new loan, you should definitely check out the following options:

Types of Student Loan Forgiveness and Discharge

Over the years the government has set up many different programs that forgive your discharge student loans under various circumstances. Student loan forgiveness programs are typically set for borrowers to participate in over a period of time, and then achieve loan forgiveness upon completion of the program. Discharges are immediate upon proving that you meet the qualifications. Anyone could decide to participate in a forgiveness program and work toward meeting the qualifications. Discharges are designed for borrowers who were either victimized in some way in the process of taking out loans or encountered circumstances later on that made it extremely difficult to pay off the loans. Read on for more information on the different options out there.

Public Service Loan Forgiveness

You may have seen some articles in the news recently about Public Student Loan Forgiveness (PSLF). It’s gotten a lot of attention because some of the qualifications are murky and difficult to navigate. But if you pay careful attention and ensure you’re following the rules, it could end up being the best option for you.

The goal of the PSLF program is to encourage college graduates to choose careers in government or non-profit sectors. If you work for a government agency or for a non-profit organization you may be able to take advantage of this program. Borrowers who do qualify can have their entire loan balance forgiven after ten years of qualifying payments.

The trick is making sure you work for a qualifying organization, that you have the correct type of loan, and that you are making qualifying loans. It’s best to verify that information up front rather than making payments for ten years only to discover that you missed a crucial piece of information. Some borrowers have made payments for ten years only to discover that they had to start all over because their payments didn’t qualify for one reason or another.

If you can avoid pitfalls though, this option may be the best for you. Once you make the ten years of qualifying payments your entire student loan balance will be forgiven. Unlike other student loan forgiveness programs, you don’t have to pay income tax on the amount you were forgiven.

While this program is rife with issues, it could be a golden opportunity for you if you’re looking to work for the government or a non-profit agency.

Teacher Loan Forgiveness

The Teacher Loan Forgiveness program is a program that incentivizes teaching at low income schools. Teachers who work for five years in a low-income school (elementary or secondary) are eligible to have their loans forgive up to a certain dollar amount. Teacher Loan Forgiveness does not forgive your entire balance like many other student loan forgiveness programs but you also qualify after a shorter amount of time.

If you meet the eligibility requirements you’ll receive a minimum of $5,000 in loan forgiveness. If you teach special education or secondary math or science, you could be eligible for up to $17,500. Many will find that Teacher Loan Forgiveness does not cover all of their student loans, but it can certainly help ease the burden.

The eligibility requirement for Teacher Loan Forgiveness are a little complicated so read about it carefully to make sure you qualify. Qualifications relate to your training as a teacher, your school’s socioeconomic level, and your total years teaching.

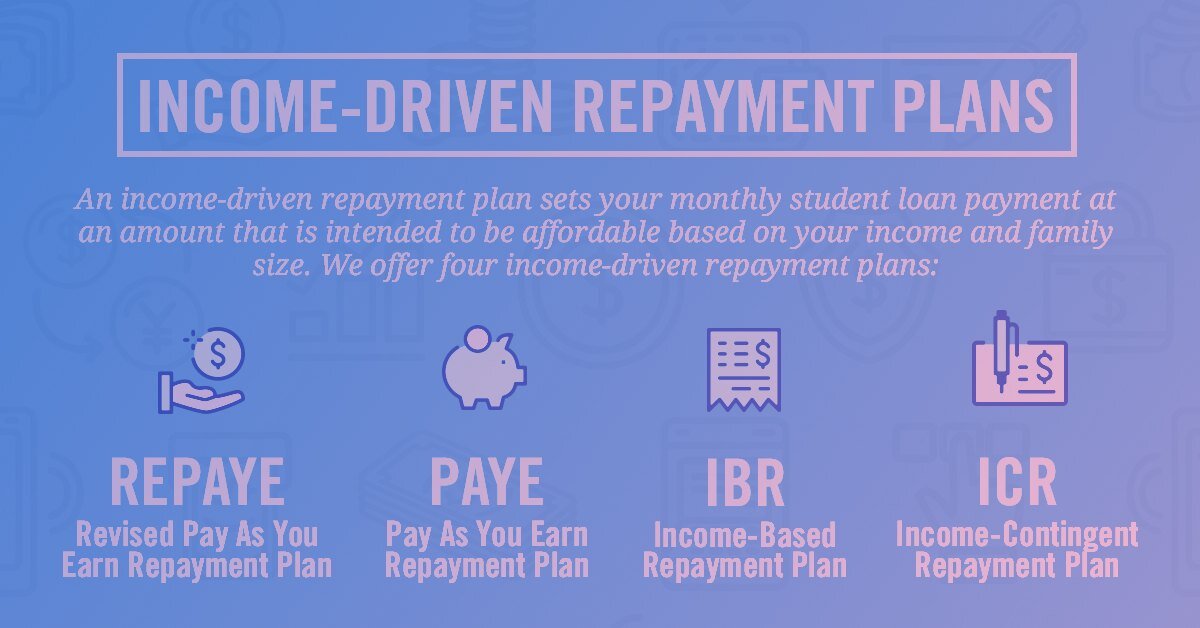

Income Driven Repayment Plan Forgiveness

One of the benefits of federal student loans is the ability to make payments based on your income rather than your loan balance. Any federal student loan borrower can request an income-driven repayment plan if their regular monthly payments are more than they can afford.

There are four different income-driven repayment plans with varying terms and eligibility requirements, but the concept is the same: your monthly payment is calculated based on how much you make during the course of a year. If you don’t have a job or make very little, your monthly payment amount could even be $0. You may end up paying down your debt at a slower rate than if you stuck to your standard payments, but you should have more breathing room financially.

Where does the forgiveness part come in? After twenty or twenty-five years (depending on the plan), your remaining student loan balance will be forgiven. All together the income-driven student loan forgiveness programs are among the most popular and widely used. One of the negatives to deciding to plan on forgiveness through income-driven repayment is that you’re signing up for at least twenty years of making student loan payments. And if your income increases during that time you may end up paying off your balance before you ever get to forgiveness.

Another downside? During the year that your loans are forgiven the discharged amount is considered income and you have to claim it on your taxes. If you had a loan balance of $100,000, you’d have to pay income tax on an extra $100,000 in addition to your regular salary. That could be a huge chunk of change.

On the positive side, however, you may end up paying much less than the amount you borrowed. If you think your income will remain low (or non-existent) for most of your career, this could be a good option for you. Even a $0 payment counts as a payment if you qualify.

Image source: Home Room

If you’re interested in income-driven repayment you can use this loan simulator to estimate your monthly payment under each plan. The different plans vary on how they calculate your monthly payment amount so your payment amount will differ depending on the plan you choose. They all set your payment based on a percentage of your monthly income, but that percentage varies. For married couples, both individuals’ incomes may be counted in some circumstances and only the borrower’s income will be counted in other circumstances. In most cases, you can switch between plans and still work toward the total time to repay. Call your servicer to discuss options, make sure you qualify, and determine which student loan forgiveness program is best for you.

Student Loan Discharge Options

There are also some other student loan forgiveness programs that you may be able to apply for depending on your situation. These are forgiveness plans you can opt in to or work toward. They’re policies set in place to protect those in certain difficult scenarios and prevent their loans from becoming an unnecessary hardship.

Closed School Discharge

If the school you’re attending while you’re enrolled and you’re not able to complete your studies somewhere else you may be eligible for student loan discharge. Qualifications for this student loan forgiveness program include being enrolled in the school at the time it closed or having been enrolled within 120 days of closing. If the school provides options for continuing your studies elsewhere you may not have the option to pursue discharge.

Borrower Defense to Repayment

If you believe you were purposely deceived by your school and took out loans because of false information they provided, you can submit a borrower defense to repayment application. For example, if the school gave you information about employment rates for graduates that are over-inflated or false, you may have a case for borrower defense to repayment. If your application is approved your loans will be discharged.

Total and Permanent Disability Discharge

The Total and Permanent Disability Discharge program forgives loans for borrowers who are considered totally and permanently disabled. The most common path for this program is to apply for Total and Permanent Disability through the Social Security Administration or the U.S. Department of Veteran’s Affairs. Once you’ve worked with one of those agencies you can use the same paperwork to apply for discharge of your student loans. You can also provide information from your physician stating that you’re unable to seek gainful employment due to your disability.

Death Discharge

If a federal student loan borrower passes away, their loans will be discharged so that their descendants don’t have the responsibility to settle the debt. Send in a death certificate to the borrower’s servicer to have their loans discharged.

Bankruptcy Discharge

Federal student loans are notorious for being ineligible for discharge through bankruptcy. However, it has happened in a few rare cases. It’s typically a lengthy and time-consuming process.

False Certification Discharge

False certification discharge applies to people whose schools falsely certified that they were eligible to receive the loan. If you didn’t meet eligibility requirements when you took out the loan, it can be discharged so that you are not responsible for paying the debt.

Unpaid Refund Discharge

When you leave school in the middle of an academic year your school should return a portion of your student loans to the government. If they fail to do that and you end up with more loans than you actually used, you can apply for discharge on a portion of your loans.

You Can Pay Off Debt Sooner with the Right Tools. Debtry Can Help.

Things to Consider

Loan forgiveness is a great thing when it works. Keep these tips in mind to make sure you take advantage of the benefits without falling into any potential traps.

Some borrowers have paid on their loans for years only to find out later that they don’t qualify for the program they were aiming for, or that some of their payments didn’t meet the requirements of the program. Whichever type of loan forgiveness you’re interested in, make sure you do your research.

In some cases, you’ll have to pay income tax on your forgiven student loans. That means that in the year your loans are forgiven you’ll get a tax statement from your loan servicer telling you the amount of extra “income” you made for the year. You’ll have to add that amount to your regular income and pay taxes on the whole thing. Depending on how much you have forgiven that could lead to a pretty hefty tax bill and you’ll want to prepare in advance. This isn’t true of all student loan forgiveness programs though, so make sure you read the fine print.

Don’t let the idea of loan forgiveness lead you to pay more over the life of your loan. If you’re working toward a loan forgiveness plan that requires you to make payments over a period of time, make sure you sit down and do the math to figure out how much you would pay overall if you were paying down debt as quickly as possible versus making smaller payments stretched over many years. In many cases, accruing interest will mean you actually pay more over a longer period. So get your calculator out (or use a fancy online tool) and calculate the best option for you.

Conclusion

Student debt can be daunting and student loan forgiveness programs may seem as real as a unicorn. But with some research and planning, it can be a reality and a real benefit. The trick is understanding the type of loans you have and which student loan forgiveness programs you qualify for.

The best way to get this information is to read the Department of Education’s literature on student loan forgiveness programs starting with StudentAid.gov. Then call up your student loan servicer to discuss your options. A servicer is a company in charge of managing your loans and they’re there to help you.

Once you’re on the right path, remain diligent and student loan forgiveness may be a reality sooner than you thought. It’s not a walk in the park, but with the right tools and information, it’s completely achievable.